How to forecast group benefits costs in Canada: A smarter guide for Canadian employers

If you’re a Canadian business owner, HR leader, or plan sponsor, you’ve probably asked some version of this question:

What will our group benefits costs be next year?

It sounds simple. But for employers, it becomes one of the most frustrating parts of planning for the year ahead.

But an even bigger question should be asked - why are these your group benefits costs in the first place?

Your benefits renewal arrives, a percentage increase is presented, and you have to make a decision. Sure, you get talked at with words like trends, utilization, or pooling. Maybe you’re even shown fancy colourful charts. After all that the answer still feels vague.

This is where most employers fall victim to the benefits vicious cycle.

They accept the new premium or go back to plan shopping to start the cycle all over again. What they aren’t shown is how these numbers connect to the thing they really care about: the cost of playing employee claims. That distinction matters.

If you want to forecast benefits costs properly and understand the metrics behind them, you can’t just skim through a renewal. You have to understand the drivers behind the numbers – it sounds difficult, but we’ll Blendify it so it’s easy to grasp.

The real starting point: benefits costs are about claims

Every employee benefits plan, regardless of structure, exists for one core purpose:

To pay eligible employee claims.

That’s the economic engine underneath the plan. Premiums are not the true end cost in themselves. They are one way of collecting money to pay claims, plus ensure the company paying the claims makes a tidy profit.

Considering all of this, it means the question isn’t:

“What will our renewal increase be?”

It is:

“What are our claims, and what is the most efficient way to pay those claims?”

That shift in thinking can change everything. Because once you separate the cost of claims from the price you are being charged to pay them, forecasting becomes strategic rather than a guessing game.

So, why do so many renewal conversations feel unsatisfying?

Most employers are presented with the renewal outcome and are rarely shown how they got there and the true math behind it.

Remember what we said in the intro. Your benefits renewal arrives, a percentage increase is presented, and you have to make a decision.

The problem is it skips the part employers need: interpretation. A useful renewal conversation should help answer questions like:

- What did employees claim?

- How much did the employer pay in billed premiums?

- What ratio was the insurer targeting?

- How efficiently was the plan structured and funded?

- Was our increase really about usage, or about maintaining margin?

Without context, these questions and the renewal report that supplements them can feel less like a forecast and more like a black box.

Now that the groundwork is set, let’s get into the renewal.

Step 1: Start with what’s actually paid

Let’s add a real-world example and work through it start to end. The first place to begin forecasting is not the proposed increase, it is the details of the current plan year.

Billed Monthly Premium | $4,466.41 |

| x 12 months |

Total Billed Premium | $53,596.92 |

|

|

Extended Health Claims | $24,472.07 |

Dental Claims | $9,772.70 |

Total Claims | $34,244.77 |

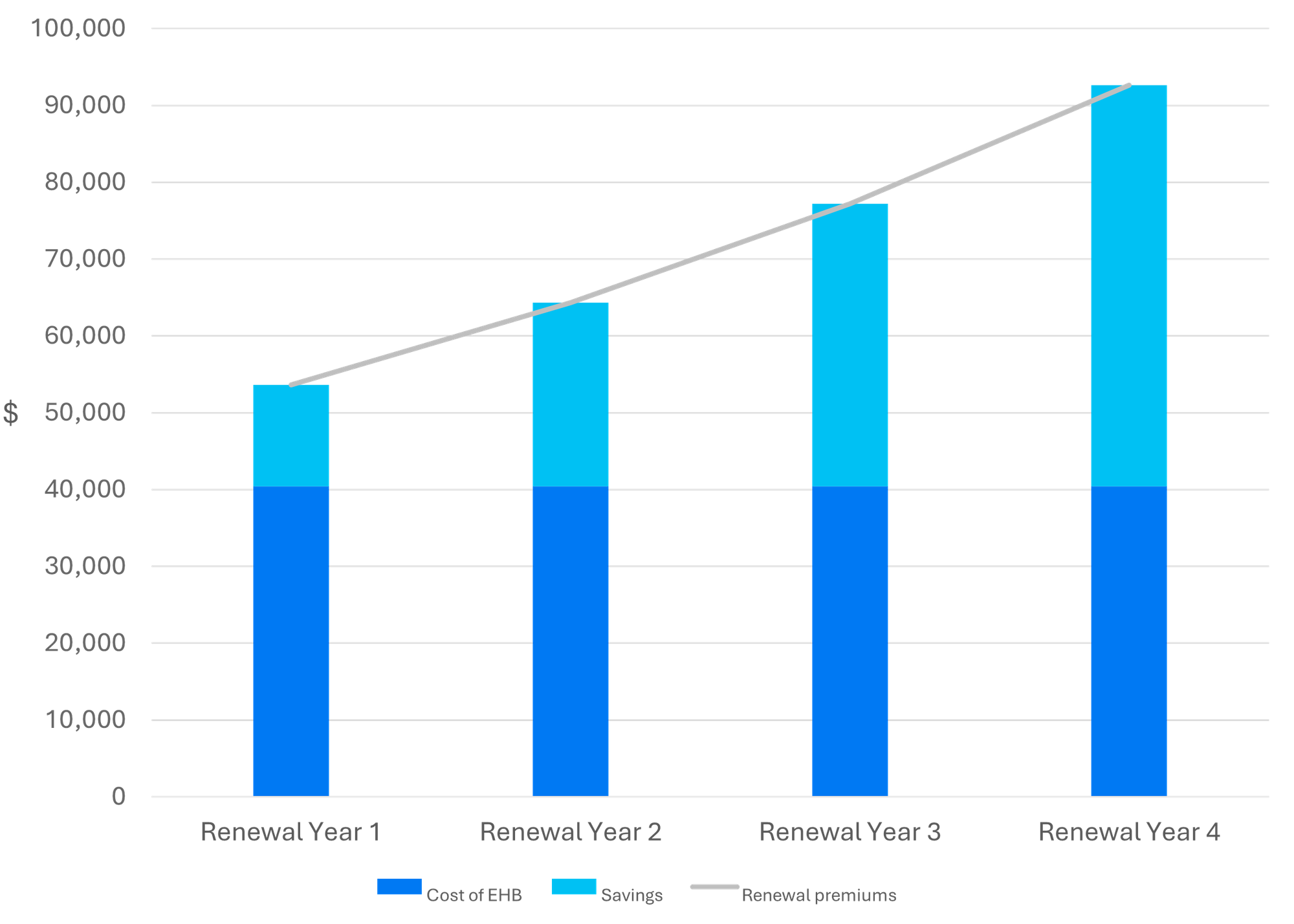

These are two very important numbers, and what you should start with when dealing with a fully insured plan. This company was charged $53,596.92 in premiums, while claiming $34,244.77. They ended up paying $21,352.15 for claims to be paid.

This is where the first question naturally arises – if claims were materially lower than premiums, what exactly were we paying for?

Step 2: Understanding the difference between premiums and claims

This is where many employers’ Spidey senses start going off.

If this company paid $34,244.77 in claims but were billed $53,596.92 in premiums, that’s like saying the insurance company charged a 62% fee to reimburse claims.

Every business needs to make money but surely claims adjudication doesn’t cost that much.

Spoiler, it doesn’t.

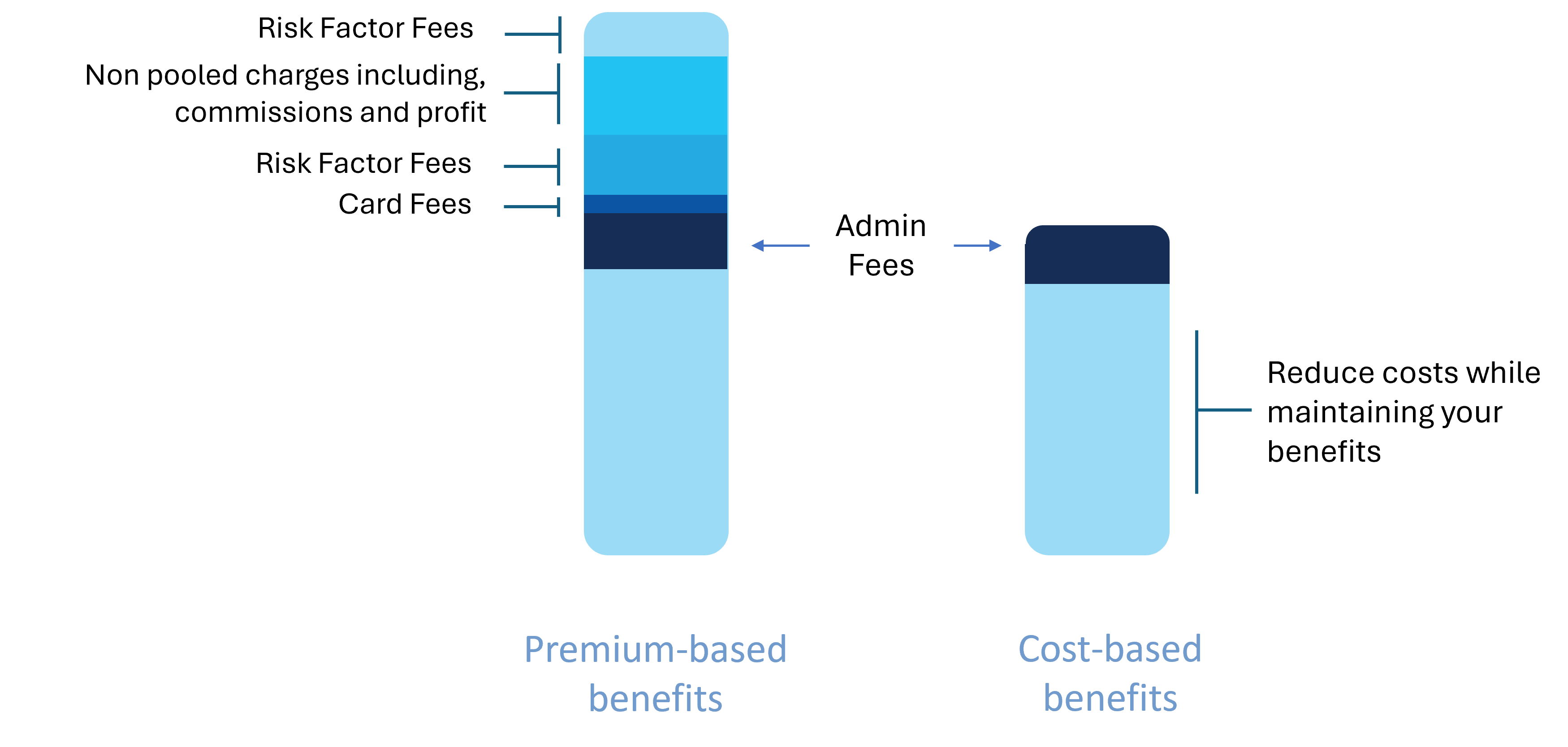

The insurance company model has all sorts of other costs baked in. Things like:

- Pooling charges

- Admin

- Margin retention

- Card fees

There is a sharp contrast between paying for claims to be adjudicated and paying for a funding model that sits on top of claim adjudication.

Step 3: Drop the “this was a one-time-thing mentality”

To put it plainly, it will never be a one-time-thing.

Things may stabilize for a short amount of time, but that peace won’t last. The reason is because Target Loss Ratio’s exist. Many employers see a term like Target Loss Ratio (TLR) in their renewal material and either gloss over it or never have it explained. But TLR matters, because it helps show what the insurer is aiming for.

At a simple level, TLR is the percentage of premium the insurer wants to pay back out in claims.

The company we’re following has a TLR of 78%, that means the insurer is effectively targeting a world where about 78 cents of premiums is used to pay claims. Let’s fit that into our table.

Billed Monthly Premium | $4,466.41 |

Target Loss Ratio | x 78% |

Target Monthly Claims | $3,483.96 |

So, to put this plainly, the company was being charged a 28% fee to pay a single claim.

Putting this all together shows that the insurer is charging 28% to cover not only their costs but line their pockets a little bit in the process. This is no accident, it’s by design.

This is why renewal conversations can feel frustrating. The employer is often reacting to a premium change without first being shown how it got there.

The worst part? This was reflective of the company’s current year. Here is the actual recommendation verbatim they received regarding their renewal:

“We propose an increase of 19% for Extended Health Care and 21% for Dental Care, for a total overall increase of 14.5%. No change has been made to pooled.

Based on our knowledge and experience we recommend accepting the renewal rate adjustment, March 1, 2026.”

Jaw dropping, right?

So, is this just cherry picking?

After seeing this you may think it’s just us cherry-picking the best example we could find to prove a point and sell our solutions. After all, this is just one example out of thousands.

That’s a fair consideration.

But the broader point still holds. Premium-based funding is not designed to make employers feel close to the raw cost of claims. It is designed to bundle claims, volatility, pricing protection, and carrier economics into one monthly number.

Still not convinced? Consider our casino analogy. When you hit the slots, the house always wins. It’s the same with group benefits, maybe one year you hit the jackpot, and you claim more than your renewals – but that won’t last for long. Your prices are about to skyrocket.

Let’s steady our focus, insurers don’t like losing money and you can be assured that if you hit it big, your next renewal is going to feel like a gut punch.

So now we understand the framework and where numbers come from. How do we actually forecast our costs?

Forecasting 101: Blendable edition

If your goal is to budget next year’s costs intelligently, here’s what to focus on.

Actual paid claims

Yup, just like above we’re getting back into claims data. What did you claim over the last 12 months? If you have the information, look into what it was broken down into, was it:

- Drug

- Dental

- Paramedical

Claim trends

This one is report dependant, but if you can take a look at whether claims are:

- Stable

- Gradual/rising

- Distorted by one off events

- Driven by a small number of members

This matters because forecasting should distinguish between normal drift and structural pressure.

Business priorities

This is probably one of the most important things to consider. Employers should be asking the question:

“What are we actually trying to accomplish when providing benefits for our team?”

Some common priorities we see in small businesses are:

- Cost control – keeping spending aligned with a budget

- Predictability – avoiding surprises (like at renewal)

- Efficiency – minimizing unnecessary fees and margins

- Flexibility – giving team members choice in how they use their benefits

- Attraction & retention – offering a competitive business experience

There isn’t a correct answer here, but the priorities you choose should shape how you structure a plan. Because once you know what matters most to your organization, you can evaluate which funding model supports those goals.

Funding models

Here is the big one. What are the ways I can pay claims? This is where the structure of the plan comes into play. In Canada, there are three main ways to pay claims:

- Premium-based

- Claims-based

- Cost-based

Each has their upsides and downsides, but we believe there is generally a more correct choice.

Ins and outs of the three ways to pay for claims

Premium-based benefits

This is the classic, run-of-the-mill plan you see within most Canadian businesses. The employer pays fixed monthly premiums, and the carrier absorbs the “volatility”. This is the model we’ve been going over thus far in the blog.

The upside is familiarity; the downside is never-ending.

Like we said, premium-based plans put Plan Sponsors into a vicious cycle that is hard to escape. Things look good initially, but once renewal hits, you’re wondering where it all went wrong.

We’ve gone over this model in depth so far, so let’s get into the next two.

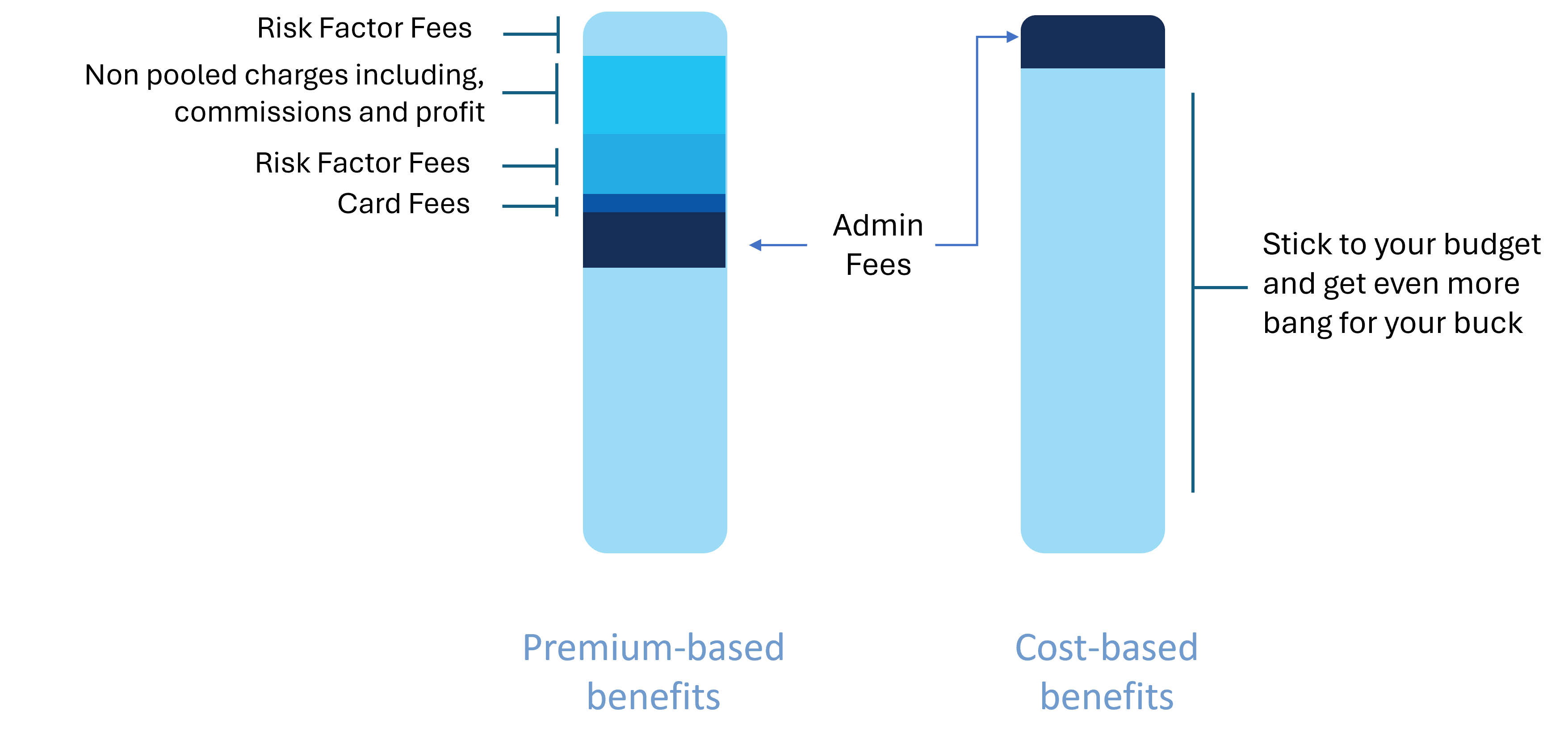

Claims-based benefits

This is you typical Administrative Services Only (ASO) plan, but we call it an Enhanced Health Blend.

It’s essentially like extended health coverage – only better. Plan members get coverage that mimics premium-based benefits, so retaining the familiarity, but the Sponsor only pays for what they use plus a small admin fee.

We’ll be frank here, this typically saves 30% of the costs a premium-based plan would run you.

The Plan Sponsor chooses:

- A reimbursement percentage

- The annual maximums

- Which practitioner or services are covered

Step by step they design the plan with us to ensure it meets all their financial and business needs. So, let’s take a look at those renewal numbers from before, and see how an EHB compares.

| Premium-Based Plan | Enhanced Health Blend |

Extended Health Claims | $24,472.07 | $24,472.07 |

Dental Claims | $9,772.70 | $9,772.70 |

Total Claims | $34,244.77 | $34,244.77 |

|

|

|

Premium/ Claims x Admin | $53,596.92 | $40,408.83 |

|

|

|

Cost to pay claims | $19,352.15 | $6,164.06 |

Ouch, it kind of hurts to look at how much money was wasted on a premium-based plan eh?

Cost-based benefits

This is our bread and butter, our Health Spending Account (HSA). You can think of it like a bank account for eligible medical expenses. The eligibility is defined by the CRA, and an explainer can be found here.

The best part? The funds put into the accounts are 100% tax deductible to the business and 100% tax-free for your team.

That means Plan Members get total flexibility over their spending with no limits or categories, get full value out of their plan, and get to utilize 100% of their compensation (because benefits ARE compensation).

For Plan Sponsors, aside from the ultimate cost control, an HSA can be used as a tool for attraction and retention while providing the most fair and equitable solution for their team.

But if we kept on going over the benefits of an HSA, this blog would be twice as long as it already is so let’s get back into our company’s example.

| Premium-Based Plan | Enhanced Health Blend | Health Spending Account |

Extended Health Claims | $24,472.07 | $24,472.07 | $24,472.07 |

Dental Claims | $9,772.70 | $9,772.70 | $9,772.70 |

Total Claims | $34,244.77 | $34,244.77 | $34,244.77 |

|

|

|

|

Billed premium/claim | $4,466.41 | $34,244.77 | $34,244.77 |

| x 12 months | x 1.18 (admin fee) | x 1.10 (admin fee) |

| $53,596.92 | $40,408.83 | $37,669 |

|

|

|

|

Cost to pay claims | $19,352.15 | $6,164.06 | $5,424.23 |

Even LESS than our EHB! If you don’t see the benefit of ditching a premium-based plan at this point, we’re not sure what else to say.

The wrap-up

Now that we’ve gone over:

- What numbers to look for in a report

- The differences between premiums and claims

- How to properly analyze the numbers

- How to forecast costs and their funding models

You should be good to go! Just remember, the question to ask when looking at costs is:

“What did our plan really cost to fund claims this year, and what structure best aligns with our priorities going forward?”

When you frame your perspective around that question, renewals and benefits budgeting become less of a guessing game and becomes purely strategic.

Say goodbye to surprises and headaches, hello peace of mind!

Remember to check us out on Facebook, Instagram and LinkedIn for more benefits bite-sized content!